If you came to my casino and you could only take home 70% of your wins, but we would absorb all losses… would you come to my casino or roll the dice in a casino with 100% gains and 100% loss? (I’d go to my casino every day!)

It may sound “too good to be true,” but there is a strategy—also a financial product—that does just that. Offered by some of the most solid financial companies in the world, it’s a contract that is guaranteed against losses. It allows you to make a “lateral move” out of the stock market into a more stable asset while still benefiting from market gains!

In this article, you’ll discover:

- The quandary many battered investors find themselves in.

- Why it may be time to exit the market now, even if your portfolio is down.

- An explanation of this strategy and how it works.

- The unique financial (and peace of mind) benefits it offers.

- The pros and cons of this strategy.

- How to get further, more detailed (and personalized) information.

Is it time to exit the stock market?

“I want to get out of the market, but I’ve got to wait for it to come back!” is a message we’ve been hearing from investors.

We understand this thinking… why sell when you’re down, right? And maybe there is another way to see things. Perhaps the question should be, “Why risk further losses in the stock market in such an economically perilous time?”

As we’ve written elsewhere (such as “The Big Short and the Next Crash” and “The War on Your Portfolio,” there is tremendous risk in the market right now. Although stock market values have recently stabilized and even risen, 2022 saw major indices drop 25% or more. Factors that could bring further pain include:

Layoffs. As reported recently in Forbes, more than half of U.S. companies are planning on layoffs or workforce reductions.

A cooling housing market. New mortgage applications have plummeted, and housing prices have slipped three months in a row. Things could get worse after the layoffs. And if you recall the Subprime meltdown, the US housing market is intrinsically tied to the larger economy.

Higher costs. In spite of some improvement, inflation is still at a multi-decade high. Elevated energy costs (and a looming diesel shortage) as well as high-interest rates mean significantly increased costs for many public companies.

A volatile international economy. Major world economies are facing big challenges. There is no resolution to the devastating Russia-Ukraine conflict. Industry in Europe has been curtailed by energy prices and shortages. China’s “zero Covid” lockdowns have sabotaged supply chains.

The economy tends to move through boom-then-bust cycles, and stock prices eventually head higher. But when will they head higher? And will a larger drop occur first?

Experienced investors such as Ray Dalio, Jeremy Grantham, and Carl Icahn believe we may be in the early stages of a much larger economic crash. Record levels of debt and an inverted yield curve—a fairly reliable recession predictor—signal trouble to come.

“Buying the dip” has become the default strategy for more than a decade. Aside from the last year and a brief 2020 “Corona crash,” it’s been largely a bull market since 2009. However, recency bias may not be your friend. When a debt-fueled bubble pops, it can be devastating. Many investors seem to have forgotten how far the market fell during previous crashes—often with deceptive “dead cat bounces” before a final bottom.

Only time will tell if staying in the market will prove to be an expensive mistake. Perhaps we have seen the start of a recovery in late 2022. Or perhaps it’s just a bear market rally that gives investors temporary hope before deeper losses.

Fortunately, there is a solution that does not require a crystal ball! If you wish to protect your principal from further downside without giving up exposure to the stock market, there is an annuity strategy worth considering.

Exit the Stock Market with an Indexed Annuity

Annuities are insurance products provided by highly-rated financial companies. They offer contractual guarantees, income riders, and (sometimes) attractive bonuses when held for minimum time frames. There are many types of annuities, and not all are created equal. However, the indexed annuity offers distinct advantages for risk-weary investors.

Indexed annuities provide upside potential based on stock market indices while protecting the principal from market losses. They are especially attractive to investors ready to exit the stock market roller coaster ride! Indexed annuities are also referred to as:

- Fixed Indexed Annuities (FIAs)

- Fixed Index Annuities

- Hybrid Annuities

- Equity Indexed Annuities (EIAs).

An indexed annuity is a safer alternative to the stock market because you don’t have to wait for a rebound in order to exit the market. You’ll still have exposure to the market—but without the risk.

Indexed annuities allow you to make a “lateral move” to an asset that stops all losses while still allowing for upside potential. If your portfolio took an elevator down and you are wondering just how deep the basement goes, you can get off the elevator now, stop further drops and catch the escalator back up!

How Fixed Indexed Annuities Work

Indexed annuities are tied to an index such as the S&P 500, Nasdaq Composite Index or the Russell 2000. However, your funds are never actually “in” the market. The insurance company invests your money in bonds and uses financial instruments such as options to manage the risk and provide guarantees.

Contrasted with a fixed annuity (which performs more like a bank CD), indexed annuities allow you to participate in a portion of the gains of a stock market index. Interest is credited only when the value of the index increases. The downside is protected and can never be less than zero. This is the “floor” of the annuity, as determined by the contract.

The upside is tempered with a cap and/or a participation rate. For instance, an indexed annuity might have a floor of zero or 1% and an upside cap of 8%. If the index has a banner year and gains 12 or 18%, you’ll be credited 8%, which is your cap. If the market gains 6%, you’ll earn 6% since that would be less than the cap.

Another way an indexed annuity contract can be written is with a participation rate. With a 50% participation rate, if the index gains 12%, you’ll earn 6%. If it earns 18%, you’ll earn 9%, and so on. If the index LOSES value, your “floor” will kick in to protect your principal. A contract can have both a cap plus a participation rate.

You would do better in the stock market in years with the highest gains. However, “securities,” ironically, offer NO security against losses! With stocks and mutual funds, there are no performance guarantees. The buyer assumes 100% of the risk–just like with the casino!

Indexed annuities are typically deferred annuities, meaning that income payments begin after the first year, perhaps several years or even decades down the road. If an annuity begins payments within the first year, it is considered an immediate annuity. Deferring payments allows for potential growth of the basis or principal. That can mean larger income payments in the future.

Income payments can last over a set number of years or can be guaranteed for your entire life, depending on the contract. Like a traditional 401(k) or IRA retirement account, investment gains are taxed only upon withdrawal. However, if the annuity is in a Roth IRA, you could receive tax-free income for life!

Fixed Indexed Annuities Pros and Cons

One thing we love about indexed annuities is that the math actually works! Although the gains are tempered, it’s not unusual for annuities to compete favorably with stocks, mutual funds, or bonds simply by eliminating the losses. Indexed annuities also tend to outperform bank CDs (although not necessarily in an individual year).

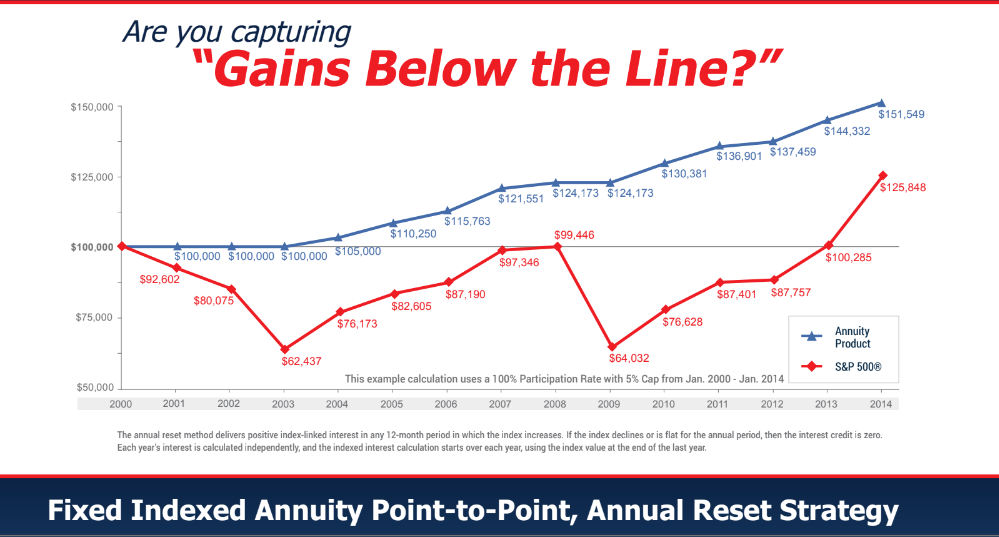

The illustration below reflects how an indexed annuity would have performed versus the S&P 500 from year 2000 through 2014, a time period with two stock market crashes. As you can see, an annuity can produce superior returns in some markets—with greater stability and no drama!

Other advantages or benefits of indexed annuities include:

Highly-rated companies. Annuities are issued by life insurance companies that have a long history of conservative management and solid performance.

No more losses! Your principal is guaranteed, and gains are locked in annually. (Even in the unlikely event that the insurance company fails, typically another insurer takes over the contract.)

Free Money!? You may be eligible for a “bonus” in your account that can help you recoup stock market losses! (Some companies began offering bonuses during the downturn and we can show you which ones.)

Income for life! You can add a guaranteed lifetime income benefit that will guarantee income regardless of how long you live. (You can start with an income rider and can graduate into a lifetime income benefit at the end of the contract.)

Extra protection. You can add optional benefits such as a death benefit, long-term care insurance, or a terminal and chronic illness rider. In this way, an annuity can provide extra protection against the “what ifs” of life for a minimal cost.

Distributions are optional. Although annuities have surrender charges, there is typically a free withdrawal option to take a percentage of income (such as 10% per year) without penalty.

No health exam. Unlike life insurance, annuities do not require a medical exam. Annuities are priced according to your age and gender, not health.

Benefits are net of fees. Unfortunately, some annuities, such as variable annuities, are known for high fees. This is not the case with fixed-indexed annuities. There are no hidden surprise fees. (You may have taxes on the gains.)

Leave a legacy. There are types of annuities that expire when you die in exchange for a higher income stream. However, most people prefer to leave the balance to beneficiaries. Indexed annuities—or, if higher, the annuity death benefit—can be left to beneficiaries.

There are also disadvantages of fixed-indexed annuities to consider. These include:

1. Surrender fees. Annuities are not designed to be short-term products and generally have decreasing surrender fees for the first 7 to 10 years. Besides surrender fees, some benefits are reduced if an annuity is not held for the full term.

2. Age restrictions. Indexed annuities are generally not available to people under age 40 or beyond 90. Many companies have smaller age ranges, such as 50 to 85.

3. Lump sums work best. Indexed annuities are not really designed for “dollar cost averaging.” Annual contributions are possible, but lump sums work best.

4. Complexity. Read the fine print, have an expert guide you, compare policies, and don’t let anybody sell you a variable annuity!

5. Reputation. Not all annuities are excellent products, and this creates a challenge. We encourage you to explore indexed annuities with an open mind (and we’re happy to help!)

6. Not inflation-adjusted. Income riders are fixed for life unless you add an inflation-adjusted rider. This should be considered in your planning.

7. Not a “complete” financial solution. Annuities don’t solve every problem, although indexed annuities are sometimes sold as a comprehensive financial solution. Indexed annuities are best combined with robust emergency funds, life insurance, and other investments.

Annuities are often misunderstood, and they can indeed be complex. However, the right annuity for the right situation can be a brilliant cornerstone of a successful retirement strategy!

Would you like to learn more?

We invite you to schedule an appointment to get more information. We’ll review your situation and put together a spreadsheet of the best options for you. We’ll pick out the top five annuities, explain the benefits and differences and “show you the money” on financial calculators!

You can schedule an appointment at your convenience right here.

We look forward to meeting you and sharing with you strategies for your continued financial success.