“Success is where preparation and opportunity meet.”

– Bobby Unser, Indianapolis 500 Champion

Do you have access to cash on demand? Or are you locking up your assets, or keeping them liquid? The answer may be influencing your prosperity more than you realize.

Most investors focus on the ROI (return on investment) of an investment or a savings vehicle. However, locking up money in investments where it is no longer liquid can actually severely limit the possibilities for lucrative returns! This is because some of the best opportunities cannot be capitalized on (literally!) without access to cash.

Cap-i-tal-ize:

(verb)

1) To provide with capital.

2) To gain advantage from.

Most accumulation vehicles lock up your dollars.

- If you put money into a retirement plan, your money stays there, sometimes for decades.

- If you save in an educational savings plan, that’s where your dollars remain until needed for tuition.

- If you invest in a business or real estate deal, your cash is locked up there for a certain length of time, or until the investment is liquidated.

- If you purchase a car with your dollars, your money is now on four wheels in a depreciating vehicle.

Usually, you have to liquidate assets or divest yourself in order to get access to use your dollars elsewhere. It’s “either/or” – you can either earn interest on your savings, earn returns on your investments, or liquidate them to spend the money, but you’ve got to make a choice.

Life Insurance: The Both/And Asset

Todd Langford of Truth Concepts financial software is fond of saying, “Most assets are either/or assets, but (whole) life insurance is a both/and asset.” This is a perfect way to describe the advantage of having an asset that can be easily used as collateral.

Cash value life insurance is a “both/and” asset. As you keep funding your life insurance policy, the cash value grows, and before you know it; you have options. Do you need money for an emergency? You’ve got it. A lucrative opportunity? Yes, you can! What about a honeymoon, a business start-up, or a down payment on a rental property? Go right ahead.

While you can simply withdraw the cash from your policy (using it as an “either/or” asset), you can also leave the cash value IN your policy – earning future dividends – and borrow against it. By accessing capital with policy loans, life insurance becomes a “both/and” asset.

Your savings continue to grow and earn while you gain access to the cash you need for an emergency, an investment, or a major purchase. Then, you can repay the loan on your own time schedule. Extra payments or a lump sum? Of course! Need to skip a couple of payments? No problem. (We do recommend that you pay your loan back diligently, as that will minimize interest and will give you access to borrow against the cash value again, should you need to.)

Financial author and speaker Nelson Nash is fond of saying, “If you have cash, an opportunity will seek you out!” Here are 5 examples of how opportunities can find you when you have access to capital:

1. Cash in on an Opportunity

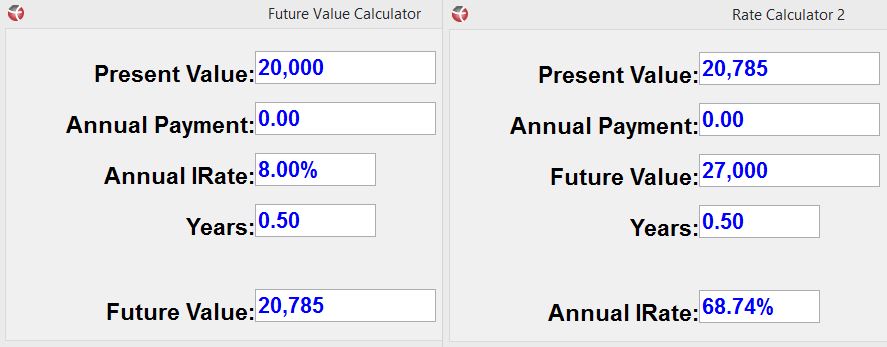

Perhaps a friend wants to sell a classic car for much less than what it’s worth to generate some quick cash. The car can fetch $30k for a patient seller in the right market, but he’ll take $20k if you can get him the cash next week. Let’s say you buy the car at $20k and resell it for only $27k. You borrow the $20k against your cash value, pay 6 months of interest at an 8% annual interest rate (an additional $785), and you sell it for $27k.

You’ve just generated a $6,215 profit or an annualized return of 68.74%!

2. Be the Bank

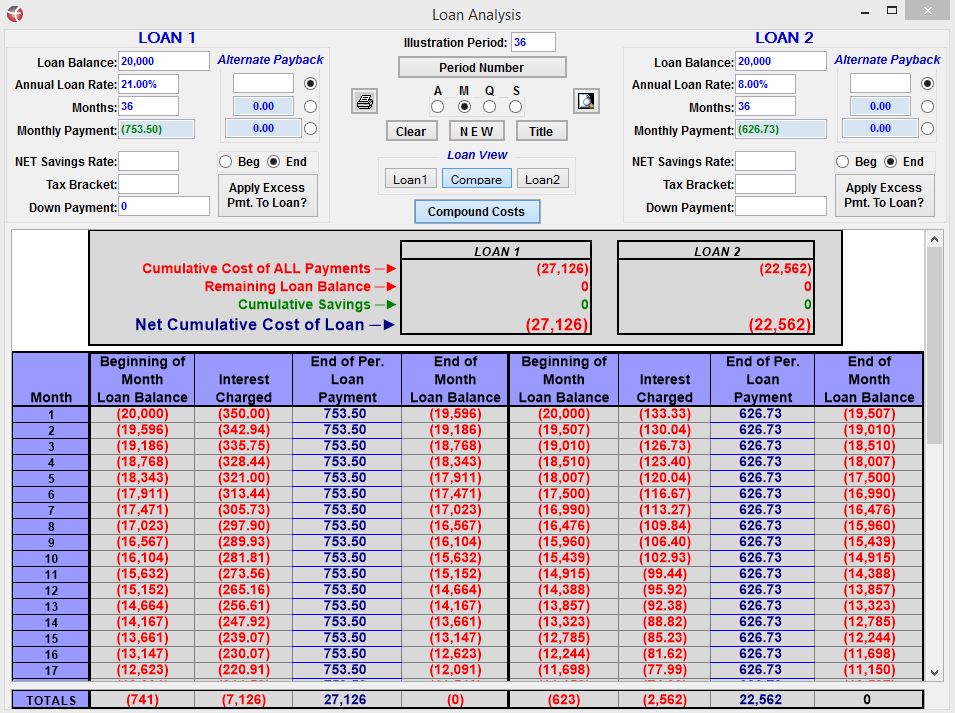

Perhaps your business needs some new equipment, and you discover that the lease on the new machines will cost you the equivalent of a three-year loan at 21% annual interest rate! Even worse, if you prepay the lease, you’ll STILL pay the steep financing fee!

You might save thousands by being able to provide your own financing in such a situation… all because you had access to cash. In the example below, a $20,000 loan (or lease equivalent) at 21% interest will cost $27,126 while an 8% interest loan over the same time period, only $22,562:

3. Earn Cash Flow

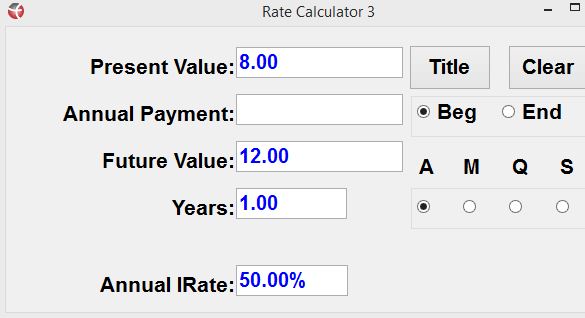

Let’s say the business equipment scenario above isn’t your business after all, but the business of a friend or family member. Could you offer to finance the equipment at a rate of 12%? It would be a fantastic savings for them, and you could borrow cash at 8% from a policy loan (no questions asked) and earn 12%.

You’d be making 50% on your money, while saving them thousands!

Don’t mistake this strategy as a mere 4% gain – 4% being the “spread” between the cost of money at 8% and the rate at which you can lend the money, or 12%. If you bought a widget at $8 and sold it for $12, it would be a 50% profit. It is the same when buying and selling cash.

4. Create an Income

When you have access to cash, you can keep your eyes and ears open for exceptional business or real estate deals that could set you up with long-term income.

One investor used his cash value to invest in cash flowing commercial real estate that generated an income for him after he was forced into an early “retirement” with a disability. His disability rider kept the policy funded, now at no cost to him. But he took it a step further and capitalized on his whole life policy. Using policy loans and the leverage of a mortgage, he was able to fund multiple real estate deals which enabled him to continue to support his family.

Learn the details of how borrowing against a life insurance policy turned an excellent investment deal from 26% gains to a whopping 111% rate of return in an article on the TruthConcepts.com blog, “How Do I Tell if my Real Estate Deal is a Good One?”

5. Take the Opportunity of a Lifetime

Sometimes, the “return on investment” isn’t financial at all, it’s personal. Perhaps it’s taking the trip of a lifetime, or checking a major item off of your bucket list.

Network marketing entrepreneur Jordan Adler had always had a dream to “go to space.” Sounds pretty far-fetched, doesn’t it? For most, it would have been an impossible dream. But when Jordan actually got an opportunity to actually book a spot on a commercial space flight (with a six-figure price tag), he said “Yes!” He knew he could access the money with a policy loan, no questions asked, and repay it at his own timing, without disrupting his other investments.

The Cost of Cashing Out

Many people consider their 401(k)s or IRAs to be their “savings.” But qualified retirement plans aren’t liquid and make poor piggy banks. You’ll pay penalties and income tax, which can gobble up nearly half of any withdrawals! In 2010, Americans paid $5.8 billion in penalties alone by tapping $58 billion in retirement funds before they were supposed to, according to a 2014 Bloomberg article.

Borrowing 401(k) monies for allowable reasons (such as a home down payment) is also deceptively expensive due to the tax treatment. You’ll have to replace those before-tax contributions with after-tax dollars, which means you can add your tax bracket rate onto the cost of the loan!

If your dollars are locked up in typical assets, you have no liquidity.

Capitalizing with Cash Value Insurance

When you have a solid, liquid asset such as life insurance cash value, you can leave that asset intact, and easily borrow against it. This leaves you with your original savings plus access to cash for your neighbor’s car, your child’s tuition, or the investment that will pay healthy returns. Best yet, your savings will keep growing, off-setting some of the interest costs. (You may even be able to use your policy cash value to obtain a bank loan at an even lower interest rate!)

You can argue that a certificate of deposit could give you the same advantage of liquidity – after all, what bank won’t lend against their own certificate of deposit? However, here again, we discover that whole life insurance is a “both/and” asset” in the way that other savings vehicles are not.

Typically, you have to choose between investments, savings, or insurance vehicles. With whole life insurance, however, you are saving and insuring at the same time. Not only will you eventually have access to every dollar put into the policy as your cash value grows, you’ll also have protection over and above the cash value the moment your first premium is paid.

In this way, life insurance is a self-completing savings strategy. Should something happen to you, the policy can still pay for your child’s tuition or supplement your spouse’s future income.

Can You Capitalize on Opportunities?

Whole life insurance is the best place we know to store long-term cash (with a permanent self-completing savings mechanism) and the best way to build liquidity for future investments, emergencies, and opportunities.

Prepare yourself for success with greater liquidity in your personal economy. Let us run an illustration for you to show you how a whole life policy can grow cash value that can be used as collateral when you need capital. Contact us today to find out more.